When a check is presented at a teller line or through your back office, our instant verification system goes into action. ChequePoint references

the encrypted information for comparison, and determines the check's authenticity before it is paid.

In the back office: When a check is deposited, the encrypted seal is read and compared with the data on the check image. If there is a

discrepancy, the suspect items are flagged and the check images and data are displayed within the ChequePoint exception summary. The

bank can then make pay/no-pay decisions, returning rejected items, thereby avoiding losses.

At the teller line: Using any check scanner, the teller simply scans the checks and ChequePoint gives an instant verification on the teller's

screen. Any discrepancies are displayed and an altered or forged check can be rejected before it is cashed.

ChequePoint

ChequePoint

Cheque Guard will implement the ChequePoint at BlueSky Bank's (or its preferred processor) Operations/Data Center.

The verification process begins with ICVS' scanning 200 dpi check images in X9.37 or .TIF files.

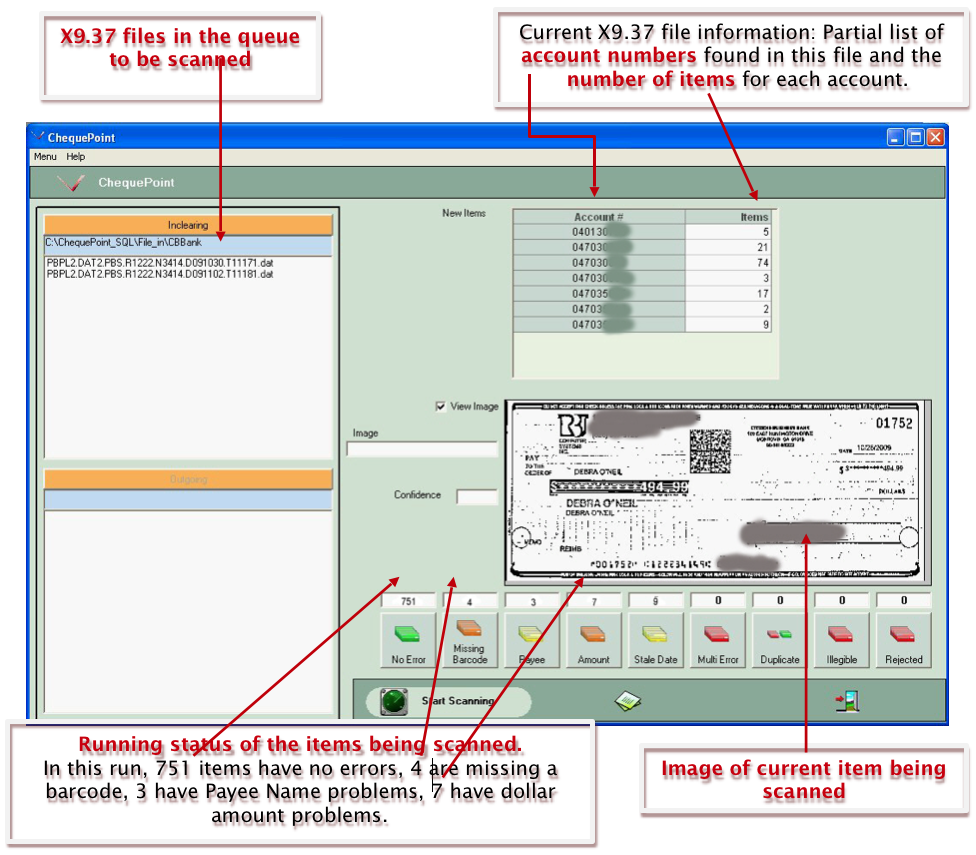

Scanning Status screen (live screen shot)

Exception Items

Exception Items

As each X9.37 or .TIF file is read, every check is scanned and all exception items are identified. These exception items are grouped by type. For example, altered payee names are grouped together, altered dollar amounts are together, and expired-date items are together. Each grouping can be sorted by high-dollar value so the high-dollar items have priority. (Because the data is self-contained, grouping can be manipulated to fit the needs of BlueSky Bank.) The operator can view each exception item on the screen and has the ability to decide to pay or return the item.

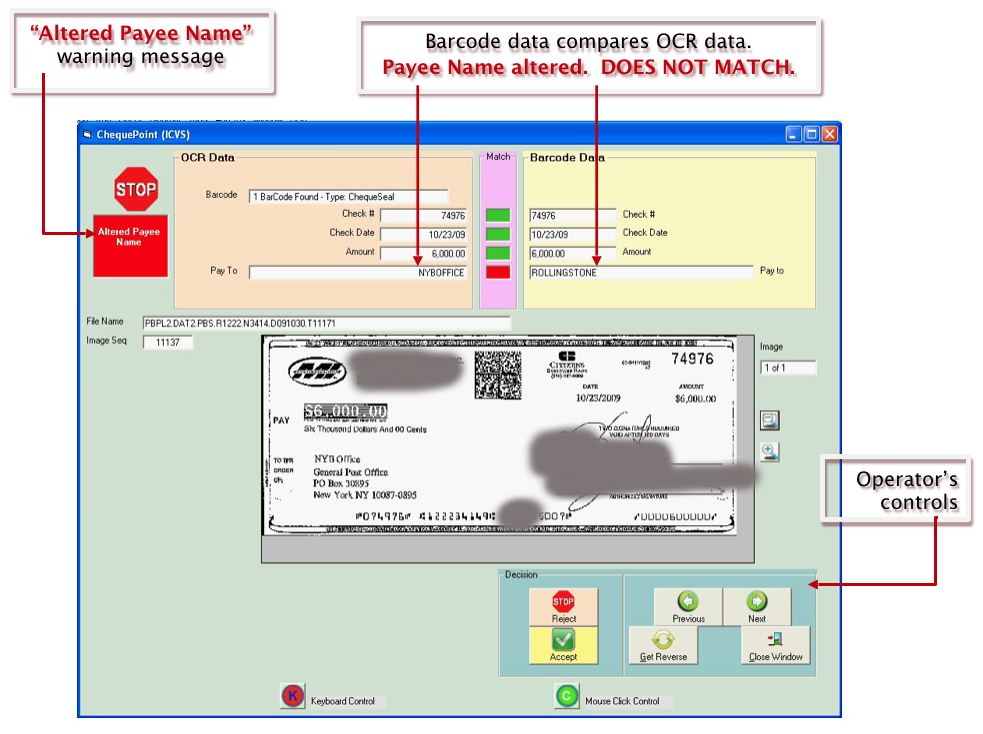

Below are actual screen shots of exception items that have been identified; the reasons vary.

Altered or Added Payee Name Exception Screen

Added/Altered Payee Names: Payee Names in the scan field that don't match are identified by the software.

Altered Dollar Amounts

Altered Dollar Amounts

The scan 'tags' every exception item, but can be set up to ignore items below a pre-established dollar amount, such as variances under $5. If the operator has time after finishing the larger items, he/she can call up 'all' the remaining items to view and resolve. Small dollar variances are often the result of encoding errors at the bank of first deposit (BOFD), or an erroneous read-and-capture error by a remote deposit user with a lousy scanner or smart phone.

Altered Dollar Amount Exception Screen

...

Staled-dated and Expired Checks

Because of stop payment and 'holder in due course' liability, it is important that customers print an expiration date on their checks. Verbiage such as 'THIS CHECK EXPIRES AND IS VOID XX DAYS FROM ISSUE DATE' should appear on the face of the check. The number of days should be kept short. Under the UCC, a check without an expiration date printed on its face is valid for 10 years. BlueSky Bank customers that purchase ChequeSuite' can automatically vary the number of days before expiration based upon the dollar amount and/or other criteria, and ChequePoint will compare the two dates. For example, a small reimbursement check for $100.00 could print 'THIS CHECK EXPIRES AND IS VOID 180 DAYS FROM ISSUE DATE.' But, a $500,000.00 check payable to a major vendor could print 'THIS CHECK EXPIRES AND IS VOID 20 DAYS FROM ISSUE DATE.' A payroll check for $1,500.00 would print 'THIS CHECK EXPIRES AND IS VOID 10 DAYS FROM ISSUE DATE.' Each check's expiration date is printed and later compared to determine if it should be paid.

'Rules' for handling exceptions are developed by BlueSky Bank when the system is installed.

Stale Date Exception Screen